When you’re buying a house, it’s important to find the best deal possible. There are many types of home loans available to you, but you’ll want to make sure that you have the money for the down payment and other closing costs. If you do not, it may cost you a lot more in the long run. However, if you can put aside the down payment, you will be able to secure a home with a lower interest rate.

First-time home buyer incentive

It’s not uncommon for a first-time home buyer to have a difficult time saving up enough money for a down payment. However, there are numerous down payment assistance programs available to help with this.

The best way to find out if you qualify for these programs is to contact an organization directly. You may be able to receive down payment and closing cost assistance from government-backed loan programs.

Federal and state government agencies and nonprofit organizations are also available to assist first-time buyers with their down payments. Some agencies focus on certain neighborhoods or home types, while others offer a variety of programs for different demographics.

Mortgage providers may also offer down payment assistance programs for borrowers. Many of these programs have income restrictions. They are also often tied to the purchase price of the home.

In addition to federal and state programs, there are also nonprofit organizations in each city and county that offer down payment assistance to low-income individuals. Check with your local real estate agent and mortgage broker to see if there are any special programs in your area.

Cash-back down payment mortgages

If you are a first time homebuyer, then a cash-back down payment mortgage may be the right option for you. You can use the money to help you furnish your new home, or pay down debt.

When it comes to getting a cash-back down payment mortgage, there are many options to choose from. Typically, lenders will offer a cash-back of between one to 7% of the mortgage. There are a few advantages and disadvantages to using a cash-back mortgage, so be sure to weigh the pros and cons before you sign on the dotted line.

The most important thing to keep in mind is that a cash-back mortgage is not for everyone. Many traditional lenders are only willing to offer them to qualified applicants, and you need a good credit score to qualify.

You might be surprised to learn that a cash-back down payment mortgage has a higher interest rate than a standard fixed-rate mortgage. That’s because the lender expects you to stick to the terms.

Mortgage loan insurance

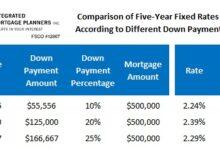

When buying a new home, you’ll need to consider the down payment. Most mortgages require a down payment of some kind. The down payment is a cash amount that you put toward your purchase.

There are many lenders in the Canadian mortgage market, ranging from big banks to smaller regional players. However, the best way to go about this is to enlist the assistance of a qualified real estate agent. They can help you get prequalified and set you up with competitive mortgage programs.

Mortgage loan insurance is a good way to reduce your lender’s risk when purchasing a new property. It also enables you to get a home with a minimal down payment. But the benefits of this may not be the same as those of a traditional mortgage.

CMHC, the Canadian Mortgage and Housing Corporation, offers mortgage loan insurance for owner-occupied properties. They also offer other mortgage-related services, such as the Home Buyers’ Plan, which allows you to withdraw your RRSP funds towards your new home.

Home Buyers’ Plan (HBP) risks

The Home Buyers’ Plan (HBP) is a program that is designed to help first-time buyers save money on their new home. It allows participants to withdraw up to $35,000 from their RRSP and use it for a down payment on a house. However, there are some risks associated with this program.

First, if you don’t make your payments on time, you will lose the tax-exempt status of your HBP. In addition, your income will drop, which can affect your consumption. This can further destabilize your financial system. You may be unable to maintain your retirement savings.

Second, you will have to pay back the amount of money you borrowed through the HBP. You must repay it in 15 years. If you don’t make these repayments, the government will tax the unpaid amount. Depending on your tax bracket, you could end up paying several hundred dollars more in taxes.

Third, your mortgage payments may be affected if you borrow more than your down payment. For instance, if you borrow more than 20% of your home’s value, you will need to get mortgage insurance.