If you are looking for ways to build your credit score in Canada, then you’ve come to the right place! There are many helpful articles out there that can provide you with information on how to build your credit score and get approved for loans and other important financial services. You’ll find information on how to repair your credit after bankruptcy and maintain a positive credit history. Also, you’ll discover tips on how to keep your credit utilization low, and you’ll see how to pay your bills on time.

Paying bills on time

A credit card with a stellar rewards program might be the ticket for your next purchase, but the best thing to do is to take a look at your bill before you dole out the cash. Thankfully, most major credit cards offer some form of payment protection, such as a grace period and extended credit card limit extensions. This is the only way to make sure you are not left out in the cold at the end of the month, and will ensure that the most important purchases go on your credit card as opposed to your checkbook. Of course, as with any consumer product, it is important to remember to keep your wits about you, lest you find yourself on the wrong side of the law.

Building a positive credit history

It is no secret that having a good credit score is essential to living in Canada. A high score will also help you get a better rate on a loan or mortgage. But there’s more to building a credit history than just racking up credit card balances. There are several steps you can take to increase your credit score, including paying off your bills on time and making purchases in your name.

The best way to start is by applying for a credit card. Many banks offer cards to newcomers. These are a great way to build up your credit score, and the best part is you can do it in your own time. Make sure you get a card with a decent limit, but don’t go overboard. You don’t want to end up with a bill you can’t afford to pay.

As a rule of thumb, a credit card with a credit line of around $2,000 CAD is a safe bet. However, it’s not a bad idea to apply for a few other cards to diversify your credit, and to keep your credit history fresh.

Keeping your credit utilization low

There are a number of factors that determine your credit score, and payment history is one of the most important. However, maintaining a healthy credit utilization ratio is another key factor in building and sustaining a good credit score.

Credit card utilization is the percentage of your total available credit that you use at any given time. Ideally, your utilization rate should be between 10% and 30%. While this may sound difficult, there are steps that you can take to ensure you achieve this goal.

Paying off your balances in full each month is one of the most effective ways to maintain a low credit utilization rate. Making a few payments early will also help. If you have trouble paying your bill on time, setting up automatic payments will help.

Keeping your credit utilization rate low will not only benefit your credit score, but it will also help you avoid paying interest. Especially when you have a hefty balance on your account, you should be careful.

Rebuilding your credit after bankruptcy

Rebuilding your credit score after bankruptcy is an important step in your financial rebuilding. It’s a project that takes time and patience. To succeed, you need to take a few proactive steps.

The first thing you should do is to get a copy of your credit report. This can be done for free. If there are any inaccurate accounts, ask the credit bureaus to remove them.

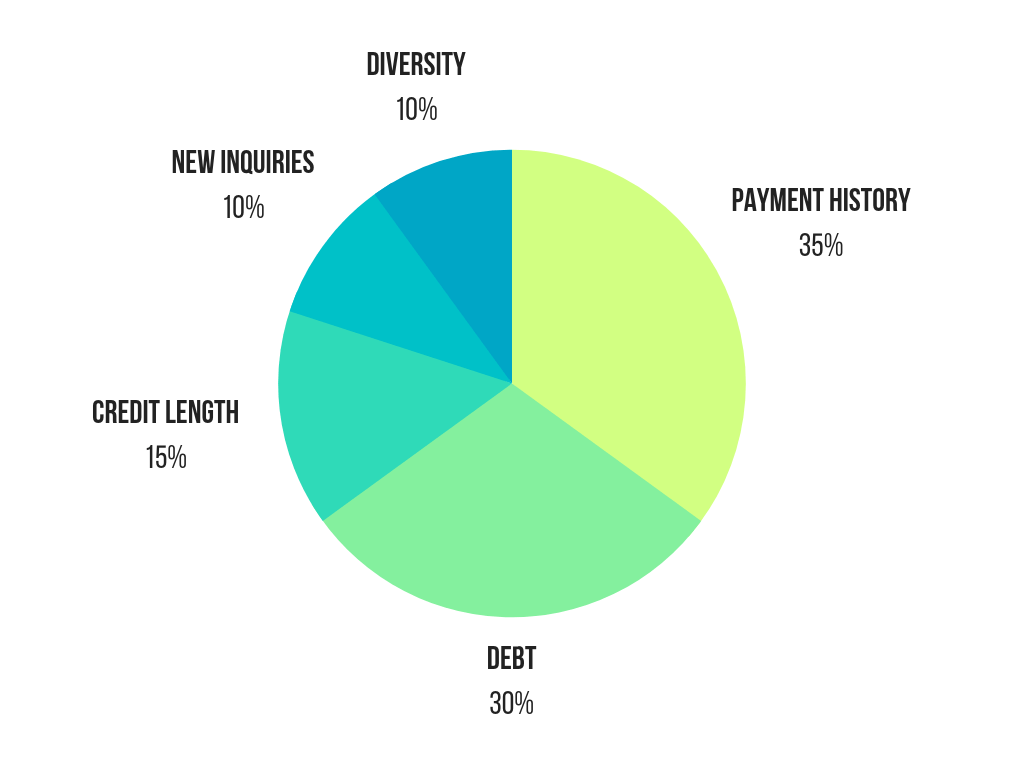

You should also make sure to pay your bills on time. When you do, you’re showing the credit card companies that you are a responsible borrower. Payment history makes up 35 percent of your FICO score.

Once you’ve established a positive payment history, you can apply for a new line of credit. However, you should limit the number of applications you make.

A secured credit card is one of the best ways to rebuild your credit after bankruptcy. Some cards even offer rewards programs. Secured cards require a security deposit to be approved.